.svg)

Use Section 179D plus utility rebates to cut lighting upgrade costs, accelerate payback, and maximize ROI; covers eligibility, timing, and required documentation.

Upgrading commercial lighting systems can be expensive, but combining Section 179D tax deductions and utility rebate programs can significantly reduce costs and increase ROI. Here's what you need to know:

Section 179D offers a federal tax deduction for energy-efficient upgrades to commercial systems, including lighting, HVAC, hot water, and building envelopes. Understanding how to navigate this deduction can help maximize your return on investment.

To qualify for the Section 179D deduction, specific criteria must be met. First, the building must be located within the United States, and the lighting or other upgrades must achieve at least 25% energy savings compared to a reference building under the Traditional Pathway or measured site energy use intensity under the Alternative Pathway.

While the deduction is typically claimed by the building owner, there’s an exception for tax-exempt entities like government agencies, non-profits, or tribal organizations. In these cases, the deduction can be allocated to the lead designer responsible for the energy-efficient property. This makes Section 179D especially appealing for public sector projects, where building owners cannot directly benefit from tax deductions.

The deduction amount hinges on two factors: the level of energy savings achieved and compliance with prevailing wage and apprenticeship (PWA) requirements. For the 2025 tax year, the base deduction ranges from $0.58 to $1.16 per square foot. Projects that meet PWA standards can earn a five-fold increase, boosting the deduction to $2.90 to $5.81 per square foot.

Additionally, for every percentage point of energy savings beyond the 25% baseline, the deduction increases by $0.02 per square foot for base projects or $0.12 per square foot for PWA-compliant projects. This structure incentivizes higher energy performance. Keep in mind that the building owner must reduce the property’s tax basis by the amount of the 179D deduction claimed. Accurate documentation is essential to calculate deductions and ensure compliance.

Proper documentation is critical for claiming the 179D deduction. A qualified individual must certify that the energy-efficient property meets the required energy and power cost reductions. For the Traditional Pathway, this means providing energy modeling reports created with DOE-approved "Qualified Software" to compare the building’s performance against ASHRAE 90.1 reference standards.

If the project is PWA-compliant, additional documentation is required to confirm wage and apprenticeship compliance. For tax-exempt entities allocating the deduction to a designer, a formal allocation letter must be provided to validate the designer’s claim.

While Section 179D offers deferred tax savings, utility rebate programs provide immediate cash rebates for energy-efficient lighting upgrades. These rebates deliver a quicker financial return compared to tax deductions. As of early 2025, about 77% of the United States is covered by active lighting incentive programs. Unlike Section 179D, which impacts taxable income at the end of the year, utility rebates typically come as upfront cost reductions or cash payments within a few months of project completion.

The rebate process has a predictable timeline. Pre-approval usually takes 2–5 weeks, and cash payments are received 10–12 weeks after installation. This means you could see financial returns within three to four months of starting your project - much faster than waiting for tax season to benefit from Section 179D. Additionally, some utilities offer bonus programs throughout the year, which can boost funding by 10% to 100% to encourage energy savings. These upfront rebates pair well with the longer-term benefits of tax deductions.

To qualify for most programs, equipment must meet DesignLights Consortium (DLC) standards. Some rebate programs also require contractors or distributors to be registered as "trade allies" with the utility. Before hiring a contractor, check their registration to ensure eligibility. Rebate programs are expanding beyond basic LED fixtures to include incentives for smart controls, occupancy sensors, and networked lighting systems. For instance, Connecticut's Energize program offers a $25 rebate for a standard 2x4 LED fixture, but the same fixture with Luminaire Level Lighting Control (LLLC) can qualify for up to $90.

Most utility rebate programs use a straightforward, prescriptive approach to calculate cash incentives. This method assigns a fixed dollar amount per fixture based on equipment type and quantity. To determine the rebate, simply multiply the per-fixture rebate by the number of qualifying fixtures. Energy savings are calculated by measuring wattage reduction (old wattage minus new wattage), multiplying by annual operating hours, and dividing by 1,000 to find annual kilowatt-hour savings. Rebate amounts for LEDs rose by 3% in 2025, with forecasts predicting an additional 10% to 20% increase through 2026.

To secure a rebate, you'll need to submit technical specifications, energy savings calculations, application forms, and detailed invoices for both products and labor. Pre-approval is essential to avoid disqualification. If your project scope or product selection changes during installation, notify the rebate provider immediately to maintain eligibility. Keep all technical data sheets and invoices on hand, as utilities may conduct post-installation inspections to verify compliance.

Section 179D vs Utility Rebates: Financial Incentives Comparison for Commercial Lighting

Section 179D and utility rebates both offer financial incentives, but how and when you benefit from them can differ quite a bit. Understanding these differences can help you better plan your project’s timeline and budget.

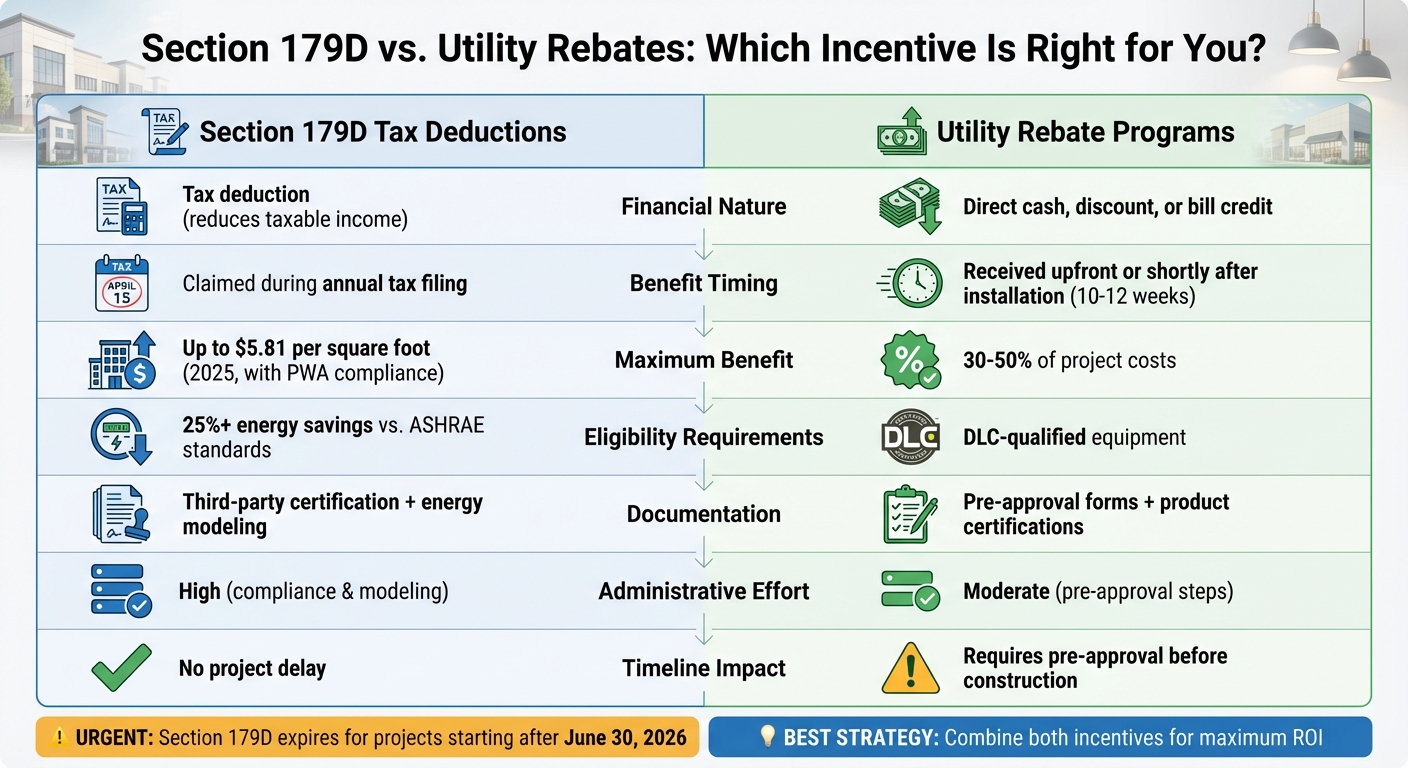

Section 179D works as a tax deduction, reducing your taxable income, while utility rebates provide direct financial benefits like cash payments, discounts, or bill credits. Timing is another key factor: the 179D deduction is claimed when you file your taxes, whereas utility rebates are usually received shortly after installation. This timing difference makes it possible to combine these incentives for a stronger return on investment (ROI).

The administrative process for each is also distinct. To claim Section 179D, you’ll need to go through detailed energy modeling and obtain third-party certification. On the other hand, utility rebates typically require submitting pre-approval forms along with product certifications. While 179D’s administrative steps don’t usually delay project timelines, utility rebates often require pre-approval before construction begins, which could affect your schedule.

Here’s a quick comparison of the two:

| Feature | Section 179D Tax Deduction | Utility Rebate Programs |

|---|---|---|

| Financial Nature | Reduces taxable income | Direct cash, discount, or bill credit |

| Benefit Timing | Claimed during annual tax filing | Received upfront or shortly after installation |

| Eligibility | Requires 25%+ energy savings vs. ASHRAE standards | Based on specific equipment or product qualifications |

| Calculation | Tied to square footage and energy efficiency | Often a fixed amount per unit or percentage of project cost |

| Documentation | Needs third-party certification and energy modeling | Requires pre-approval forms, receipts, and product certifications |

| Administrative Effort | High due to compliance and modeling | Moderate, with pre-approval steps |

With Section 179D set to expire for projects starting after June 30, 2026, it’s essential to factor in these timelines when planning. At the same time, utility rebates are expected to increase by 10% to 20% for LED-related projects through 2026. Taking advantage of both incentives while they’re available can maximize your project’s financial benefits.

With some strategic planning, you can make the most of two separate incentives: utility rebates and 179D tax deductions. The key is to align their timelines effectively - secure utility rebates before starting your project and claim 179D deductions when filing your taxes. A well-structured plan ensures your project benefits financially from both.

Start with an energy audit, which typically takes about a week. This step establishes a baseline and provides the data needed for both utility rebate applications and 179D certification. After the audit, spend 3–5 days identifying energy-saving measures that qualify for these incentives. Submit your utility rebate applications at least 2–3 weeks before beginning any physical work, as pre-approval is often required.

When selecting equipment, go for DLC-qualified LED fixtures with high lumens-per-watt efficiency and integrated occupancy or daylight sensors. These not only meet rebate criteria but also help achieve the 25% energy savings required for 179D deductions. By 2026, eligible projects could claim up to $5.94 per square foot under 179D, while utility rebates may cover 30–50% of your project costs.

Federal law requires a qualified third party to handle 179D energy modeling and certification, which must be verified by a licensed engineer or architect. Companies like Luminate Lighting Group can simplify this process. They manage everything - from full-building energy modeling and on-site inspections to compliance documentation. Additionally, they coordinate with your tax professionals to ensure all requirements are met. By also handling your utility rebate applications, they streamline what could otherwise be two separate and time-consuming processes. This coordination reduces administrative headaches and keeps your project on track with both incentive schedules.

These incentives can slash taxable income by up to $5.94 per square foot (if prevailing wage and apprenticeship requirements are met) and cover as much as 50% of project costs. This can dramatically shorten payback periods and free up capital for other improvements.

But there’s a catch: these benefits won’t last forever. Under the One Big Beautiful Bill Act, projects starting construction after June 30, 2026 will no longer qualify for the 179D deduction. Jennifer French, Partner at PBMares, highlights the urgency:

"Section 179D, a widely used deduction for commercial building improvements, will not be available for projects that begin construction after June 30, 2026. That means contractors and building owners only have a limited time to claim the benefit".

Since energy modeling, site inspections, certifications, and documentation require careful coordination - and can take months to complete - it’s crucial to start early. Committing at least 5% of total project costs well before spring 2026 ensures you’ll meet the deadline.

To make the process smoother, building owners should consult tax advisors and engage qualified energy modelers as soon as possible. Firms like Luminate Lighting Group streamline the process, handling both 179D certifications and utility rebate applications. This reduces administrative headaches while ensuring all technical requirements are met and deadlines are achieved.

The clock is ticking. Starting now can secure upfront cash rebates and long-term tax savings - a smart move for any commercial property owner looking to maximize these incentives.

Yes, it's possible to combine 179D tax deductions with utility rebates for the same lighting project. By using both incentives, you can lower the initial project costs while boosting your return on investment (ROI). This approach not only reduces upfront expenses but also enhances long-term savings.

The 179D June 30, 2026 deadline hinges on the definition of the "start of construction", which generally means the formal beginning of physical construction work. This timing plays a crucial role in establishing a project's eligibility for the deduction.

To make sure you don't miss out on your 179D deduction or utility rebate, it's crucial to keep thorough records. Important documents include energy audits, certifications showing energy savings, and third-party verification for the systems you've installed. For 179D deductions, especially on government projects, you'll also need an allocation letter from the building owner or relevant authority. All your documentation should clearly demonstrate compliance with IRS standards and energy savings criteria to safeguard your tax benefits and rebates.